It is hard to fathom what the early days of the 21st century globalisation era were like: the bare existence of e-commerce, the monopolisation of local (or at most regional) products, and the months-long international shipping.

However, with current disruptions in the global supply chain, the international shipping industry, and global manufacturing, it seems we have returned to a state akin to the past.

This serves as a strong reminder of how far globalisation has come and how quickly it can all crumble.

How the Global Supply Chain Crisis Came About

Nothing is infallible. The global supply chain is neither the rule nor the exception — it is the prime example. Forged by the drive of capitalism and globalisation, the global supply chain is the interconnection of many stakeholders of many different levels and sectors. It is easy to see how one cog in the machine could either make or break the production.

World Trade General Ngozi Okonjo-Iweala highlighted at the World Trade Organisation’s Global Supply Forum that the supply chain infrastructure “was not built for a world where a climate disaster can interrupt factory operations worldwide or a microscopic virus can upend the movement of goods and services and people almost overnight.” But of course, the world we live in is not rid of these.

Climate disasters have impacted natural resources, crops and trading routes. Floods, scorching heat and wildfires have also become increasingly rampant. India has been facing such intense heat that crops are unable to grow, and droughts in Brazil and Africa have also affected crop growth and harvest yield.

Rising sea levels and extreme weather conditions also pose potential problems in destroying transport infrastructure and affecting trading routes.

On the point of a pandemic, COVID-19 is no stranger. The global supply chain has been affected by this in many ways: a sharp increase in demand for physical goods that pushes transport, infrastructure and manufacturing systems over the limit; labour shortages; resource shortages; price hikes etc. Countries moved into lockdowns, international travel grinded to a halt and international shipping durations significantly lengthened.

But climate change and a pandemic are not all. Sharing the same sentiments as General Ngozi Okonjo-Iweala, JP Morgan adds that geopolitical tensions and conflicts are other sources of problems.

The Russian-Ukraine conflict has thrown a wrench into any recovery or progress from the global easing of COVID-19 measures. To begin with, Russia and Ukraine produce 28 per cent and 15 per cent of the global supply of wheat and maize respectively. Russia is also a treasure trove of gas and oil.

However, with countries responding to this conflict by imposing unilateral sanctions, most of them soon find themselves entangled in a larger global supply chain crisis.

A Look Into What Is Happening

The World Trade Organisation (WTO) outlined the problems resulting from the vulnerable global supply chain at the Global Supply Chains Forum focusing on ‘Easing supply chain bottlenecks for a sustainable future’ held on March 21st, 2022.

These problems include higher transportation costs, traffic congestion and delays, labour and skills shortages, lack of digital technology accessibility and a lack of availability of affordable trade finance.

The aggravated transportation issues were attributed to the imbalance between the production and demand of goods from countries imposing lockdowns and reopening at different times, as well as the scaling back on production from shipping companies.

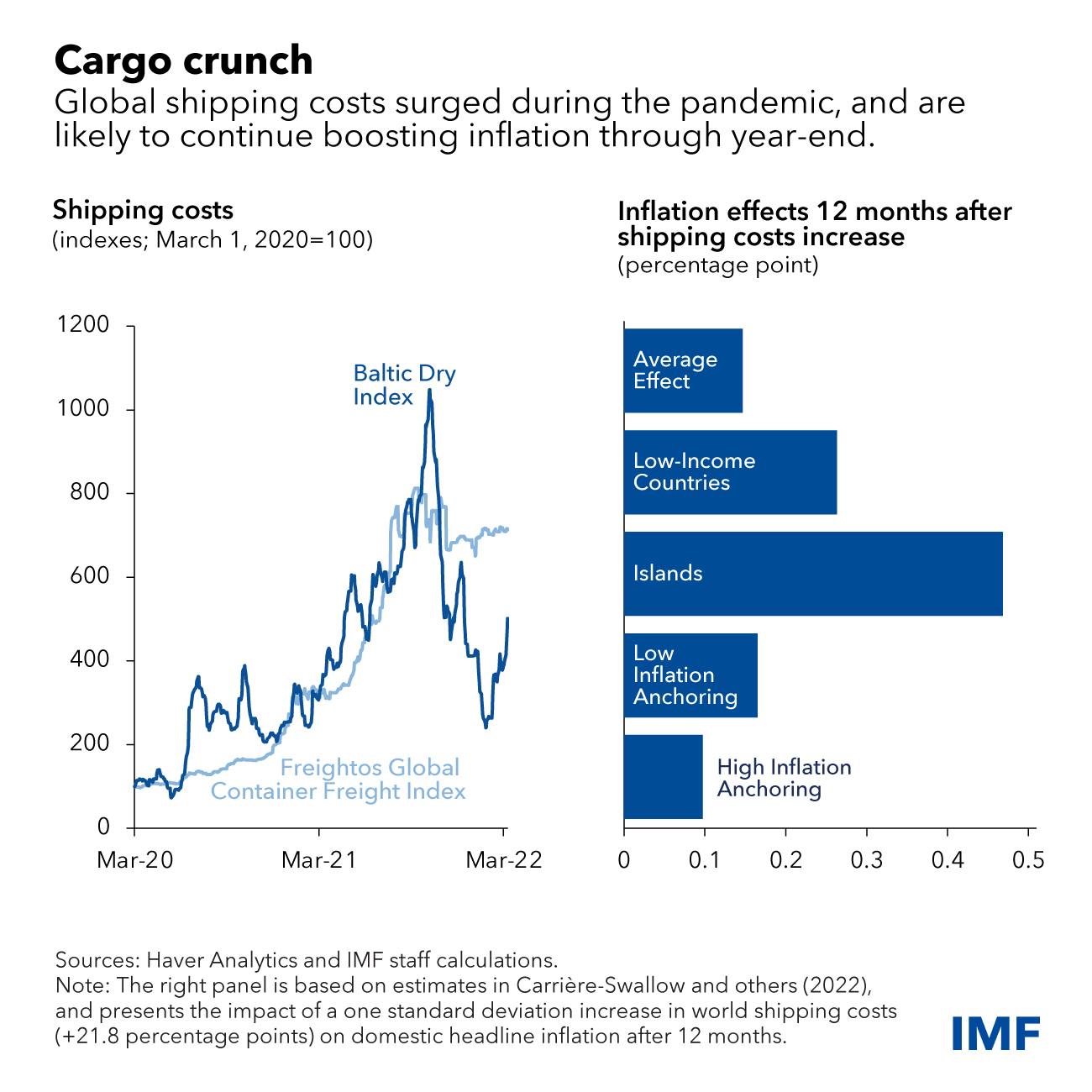

Global shipping costs in particular are predicted to continue rising despite most countries easing their COVID-19 safety measures and adopting a post-pandemic approach, according to Dutch multinational banking and financial services corporation ING’s THINK. Blank sailings (cancelled port calls) also remain a thorn in the global supply chain side that contributes to more delays and congestion, resulting in the overall shipping performance reaching the lowest it has been in ten years.

In addition, the ongoing Russia-Ukraine crisis and China’s sudden lockdowns in alignment with their zero-COVID strategy further disrupt trading routes, amplifying the instability and uncertainty of the global supply chain and its immediate effects.

With the global economy barely recovering from the effects of the pandemic, which saw many countries switching major trading partners, some exporting more goods than before the pandemic and some still struggling to meet pre-pandemic export quotas, it is thrown back to square one.

Besides disruptions to transport and therefore trade, the world is also experiencing a global labour shortage even though countries are making an effort to stabilise their markets and return to pre-pandemic production levels. This is evident in Europe, Australia and Singapore where job vacancies are at 1.2 million, 400,000 and 92,100 respectively.

A report from Korn Ferry, a management consulting company, finds that more than 85 million jobs could go unfilled by 2030 because of structural issues which refers to not having enough skilled people to take these jobs up.

There are four main reasons for the global labour shortage. The COVID-19 pandemic, for one, caused millions of deaths, millions of others to struggle with the long-term effects of the virus, and many more to deal with exacerbated mental health issues.

Low wages in the face of the worsening economic outlook also spurred workers to seek higher paying jobs leaving those lower wage jobs empty. To make things worse, the global ageing population coupled with low fertility rates further shrinks the already decreasing working population.

Not to mention, the pandemic saw a boom in the technological industry, which led to a larger technology skills gap as many workplaces integrate advanced technology, artificial intelligence and automation.

Another effect of the disrupted global supply chain includes shortages in these areas: raw materials, food, and final products. In response to uncertainties, many countries took on an isolationist approach, almost completely shutting off their trade.

For example, India ended up banning wheat exports as the heatwave burnt output and domestic prices rose. Ukraine closed its port when Russia invaded, depriving the world of its grain supply. Indonesia, the world’s top palm oil producer, stopped exporting palm oil.

Diving deeper: Receptiveness of Countries

It is not shocking that the less developed economies get the shorter end of the stick. From facing high export barriers to difficulty obtaining inputs, it is not an exaggeration to say that their economies are now riddled with more problems.

Experts at the United Nations Commission on Population and Development’s 55th session warned that the developing world is at the cusp of a “perfect storm” of debt, food and energy crises.

Sri Lanka is one such victim. It is said that contributors to Sri Lanka’s economic problems are deeply rooted in the government’s gross mismanagement. Effects of their disrupted economy include: exams being cancelled due to print paper shortages, prices of essential goods tripling, and power outages lasting for about 15 hours. Worst still, these problems are just the tip of the iceberg.

Nevertheless, the precarious continued existence of the economy relied on its tourism and foreign exchange based on remittances. Tourism accounted for 22 per cent of Sri Lanka’s total Gross Domestic Product (GDP) in 2019. Workers would work overseas and send back foreign currency to their families. But, when COVID-19 hit, this main way of sustaining its economy was lost, and it changed everything.

Its US$7.9 billion (S$10.5 billion) worth of foreign reserves in 2019 drastically dropped to US$1.6 billion (S$2.2 billion) by 2021. This significant drop in foreign reserves is accredited to Sri Lanka’s economic policy of overvaluing the rupee to make imports more affordable.

The artificial exchange rate, which the government is struggling to maintain, is normally maintained through the buying and selling (or borrowing) of foreign currency which Sri Lanka is desperately running out of. This means the country is struggling to buy enough imports, and the people’s money is worth much less each day. The economic fallout is visible, tragic, and exemplifies the gravity of the ongoing crisis. But of course, this is just the shorter end of the stick.

The best case scenario of the ongoing crisis would be what the more developed countries are experiencing. Currently, they have mostly either been in recovery from the crisis or have come up with a rough game plan to tackle the crisis, thanks to their existing resources and power.

The biggest threats for them mainly revolve around the Russian-Ukraine conflict and China’s strict adherence to a zero COVID strategy.

The Russian-Ukraine war threatens the energy supply because many of these more developed countries rely on Russia’s monopoly of natural gas.

Rising inflationary pressures and an increasing risk of recession are already happening. The prices of essentials have gone up, and the recent euro-dollar parity does not indicate good news for Europe and their efforts to lower inflation rates.

In the case of China, not only does China account for an estimated 12 percent of global trade, it is home to many key shipping ports: Shanghai, Shenzhen, Qingdao Tianjin, Guangzhou, Xiamen, Ningbo and Dalian. China’s lockdown earlier in June only worsened the bottlenecks in Asia, making the situation“somewhat worse than we anticipated”, said economists at Goldman Sachs.

However, some of these more developed countries have already managed to adapt to a global supply chain crisis. Take, for instance, Singapore’s pivot to frozen chicken meat and looking to Indonesia for imported chicken supply when Malaysia banned their export of chicken to Singapore to address domestic shortages.

Singapore’s economic recovery remains on track despite a slowdown from its major trading partners, strong inflationary pressures and the Russia-Ukraine conflict, and possibly independent of the effects of the pandemic. The year 2021 saw its gross domestic product (GDP) grow 7.6 per cent despite the 7.2 per cent estimate and a 4.1 per cent contraction in 2020.

Ravi Menon, the managing director of the Monetary Author foretells: “The extent of the growth moderation will depend in part on how the scenarios for the global economy will pan out. As of now, we expect neither a recession nor stagflation in Singapore next year.”

However, the structural weaknesses of the global supply chain have already existed before the pandemic and mayhem we see today. The biggest weakness is its vulnerability to shocks. Now, more than ever, is the push to fortify the global supply chain to make it more resilient.

More that can and should be done

Sometimes when there is a fire engulfing your house, the only comfort is brainstorming remodelling plans — solving all the problems with the old house. The dramatic analogy aside, the principle still stands: the global supply chain is in dire need of revamping.

A crucial step to preparedness is to strengthen automation. Now is not the time to debate against technological advancement, for the last time to embrace it might just be passing by.

Singapore is capitalising on a USD14 Billion (S$20 billion) highly automated Mega-Port. Singapore is one of the busiest ports connecting Asia to Europe and is planning to build the world’s biggest automated port by 2040, doubling its existing space and featuring drones and driverless vehicles. This addresses the problem of bottlenecks: adding capacity and increasing speed.

Choi Na Young Hwan, head of the international logistics analysis team at the Korea Maritime Institute said: “Singapore is setting itself as a benchmark for other ports.”

The global supply chain crisis is also the perfect time to bridge the gap between developing and developed countries. There is currently a US$1.8 trillion (S$2.5 trillion) trade finance gap that is stopping the integration of developing countries, small medium enterprises (SMEs) and women-owned businesses into supply chains.

Cross-border payments, open-account trade finance and documentary trade transactions are areas experts should also be leveraged to boost trade, according to the WTO’s Global Supply Chains Forum.

Adding on, Seedy Keita, Minister of Trade, Industry, Regional Integration and Employment of The Gambia, reported on the development of the Pan-African Payments and Settlement System (PAPSS) and how it is key to fostering regional trade under the African Continental Free Trade Agreement (AfCFTA). PAPSS is a cross-border, financial market infrastructure enabling payment transactions across Africa.

Hence, despite having entered one of the darkest tunnels in economic history, at least there is still a glimmer of hope. The world recovered from world wars, the 1997 Asian Financial Crisis, the cold war, the 2008 financial crisis, and numerous pandemics. The upheaval from the pandemic with its unprecedented ripple effects has seen signs of recovery just after two years. It will be a bumpy ride, but the light is there, no matter how faint it is.