An Unlikely Consensus

Emerging from the fog of uncertainty, world leaders had come to a small — but important — consensus at Conference of the Parties (COP) 27 of the United Nations Climate Change Conference (UNFCCC). Nothing short of a breakthrough, COP27 closed to countries agreeing to a Loss and Damage (L&D) fund for countries ruined by climate catastrophes.

The host this year, Egypt, is no stranger to the stupendous vexations of weather patterns. In fact, the Nile Delta, the Intergovernmental Panel on Climate Change (IPCC) reports, is at extreme risk of coastal erosion, land loss, disease spread, water conflict, and much more.

A relic of a past we cannot conceive, the nilometer was a construction that allowed ancient Egyptians to determine the level of water during the Nile’s annual flooding season. Measuring it allowed them to determine the year’s harvests and the locale’s taxes to be collected. The nilometer indicated famine if the level was too low; destruction, if the level was too high; and if it was just right, flourishing and good harvests. Where water moves, so does civilisation.

The nilometer, obviously, is a contraption not in use anymore. However, it represents the protohistory human-nature struggle. The struggle that continues to this day as extractive rapacious planetary industrialisation has thrown us into crisis after crisis. The struggle that has now culminated in what economists are calling a polycrisis.

The climate crisis, COVID-19, supply chain shocks, inflation, slowing growth, sovereign debt crises, energy shocks, rising interest rates, and even a third world war: “Welcome to the world of the polycrisis”, Economic historian Adam Tooze writes. Interconnected crises connect our world. Wow, we truly are living in a global village! Unfortunately, the fallout from the polycrisis will disproportionately affect the less-privileged Global South.

Low-income countries like Sri Lanka and Pakistan have an extraordinarily high level of debt. This has thrown them into the maelstrom of polycrises. As a result of more expensive borrowing, low-income countries (e.g. Small Island Developing States, parts of South Asia and South America) that depend on the international reserve currency cannot finance projects and programs to put out the blazing debt fire.

What is to be done?

The Bridgetown Initiative

On the panel Money and the Climate Crisis organised by Phenomenal World, academics discussed the tenuous link between polycrises and debt. Avinash Persaud is an academic and economic adviser to Mia Mottley, the President of Barbados. What many saw as a win at COP27 had, in fact, been the direct result of the imagination of the Barbadian convoy. Enter the Bridgetown Initiative. Broadly speaking, it refers to a reform of the global financial system.

Specifically, Barbados outlines five points for reform. One, the exercise of developed countries’ influence to convince multilateral development banks (MDBs) and the World Bank (WB) to provide US$1 trillion (S$1.35 trillion) for financing in climate and development. Two, the delivery of promises to provide emergency liquidity via the use of US$100 billion (S$135 billion) in Special Drawing Rights (SDRs), an international reserve asset and an accounting unit for IMF transactions. Three, the creation of a Loss and Damage (L&D) fund to endow those ravaged by the climate crisis with capital to rebuild. Four, the use of more imaginative funding mechanisms for capital. Five, aligning incentives for the engagement of the private sector.

To this end, Persaud has an optimistic view where he sees the establishment of the L&D to be “historic” and “unprecedented”, considering the “variety within the G7 plus China” along with “a 39-member alliance of small island states”.

SDR Redistribution

Shedding some light on the state of global finance, Mona Ali from the State University of New York New Paltz highlighted that our current monetary regime is characterised by almost complete dollar hegemony. “60 per cent of foreign exchange reserves of nations — about 40 per cent of capital easing, you know, we’re talking about equity and debt — is dollar denominated.”

Ali points out a salient point that a breathtaking amount of capital is sitting untouched in the form of SDRs. According to research from Stephen Paduano from the London School of Economics, “US$992 billion (S$1.34 trillion) in SDRs remain idle in the reserve accounts of IMF members’”. This is due to the nature of SDRs which had, in 1970, been created and allocated to International Monetary Fund (IMF) members according to their quotas. What is an IMF quota? It is a function of Gross Domestic Product (GDP), openness, variability, and reserves, that determines prospective resource contributions, voting power, access to financing, and of course, SDR allocation. From this, we can see how quotas inadvertently benefit developed economies (DC) disproportionately, and marginalise the less developed economies (LDC). Due to the fact that DCs need not use this capital because of their better-oiled economies, almost US$1 trillion remains unused. As Paduano points out, the SDR utilisation rate difference between DCs and LDCs are 42.9 per cent and 5.9 per cent respectively.

Ali regards regular issuances and redistribution of SDRs with utmost importance. In line with the Bretton Woods regime in 1944, under which the IMF was created, she says that “SDRs can be an important source of debt-free liquidity to finance the clean energy transition.”

Persaud said, “Our plan is a global climate mitigation trust seeded with $500 billion (S$674 billion) of SDRs. If you issue your own reserve currency, you don’t need an SDR.”

“The idea is that, that will allow us to put equity into developing country projects — equity, not debt — and that will leverage something like two to $3 trillion (S$4.04 trillion) of private sector finance.” He added.

Against this, Brad Setser, Whitney Shepherdson Senior Fellow at the Council on Foreign Relations, says that the SDR allocation mechanism means SDRs are practically permanent loans to the country of distribution. He notes that if an asset is given away, the liability remains. Instead, Setser opines that SDRs should be mobilised more creatively outside of the constraints of the IMF.

“SDRs are technically a perpetual liability, and they do carry a non-trivial interest rate.” He says that it could be leveraged “as a perpetual loan, in some sense to various institutions, which then can lend at the SDR interest rate. Thinking of it as cheap debt financing strikes me as the easier approach to achieving results quickly.”

Scaling Up Multilateral Development Bank Lending

On that note, Rishi Ram Bhandary, Assistant Director of the Global Economic Governance Initiative at Boston University, spoke about the need for MDBs to step up their efforts in climate financing.

Drawing on the example of Egypt, he says that solving for stability hasn’t been impeded by a lack of imagination but rather the lack of financing. There is a link between debt and climate ambition.

“You saw a country like Egypt, the host country of this COP, saying very clearly in their pledge that they are unable to make a stronger pledge because of the fiscal constraints,” Bhandary said. “They are so much in debt, that they are not actually able to enhance their ambition.”

Scaling up MDB lending is the key for him; “If you don’t increase the balance sheets, in a much more meaningful way, the scale of finance that needs to be mobilised, it’s simply not going to happen.”

Managing Endogenous Factors

Providing a contrary viewpoint was Anna Gelpern, Anne Fleming Research Professor at Georgetown Law. On one hand, she does support creativity in financing, and that “debt is a social institution, social construct, accounting concept”. However, she notes that resource lack is markedly not, “be it for climate adaptation, loss and damage, hunger, war.” Creativity doesn’t mean ignoring the real challenges that exist independent of financing. As she puts it, “One of these crises is not like the other. Drowning in debt is a metaphor. Drowning in water is not a metaphor.”

Adding on, she says that focusing just on financing simply is not enough, there has to be a focus on structural problems. “Nobody wants to talk about what happens the day after you drop the debt. And five years after you drop the debt — look at HIPAA countries, right? — More than half of them are back in debt distress.”

Persaud added on to this, calling attention to how the high cost of capital in LDCs dissuades the private sector. He sees the risk that the private sector faces as fundamentally systemic. “When you have an international reserve currency and there’s a global crisis, your currency goes in high demand that allows you to have activist fiscal and monetary policy. When you don’t have an international reserve currency and you’re in crisis, your currency is collapsing, you’ve got to tighten monetary policy in a tighter fiscal policy. It’s a totally different environment, and the private sector can’t mitigate that.”

The solution to this, in his view, is the deployment of SDRs: “a proxy of this international reserve currency to help us reduce that cost of capital.”

A Third Balance Sheet

What he refers to as the “third balance sheet”, is a trust. To this, Persaud raises the example of the Global Climate Mitigation Trust (GCMT) discussed at COP27. The trust, still in its proposal stage, will hold US$500 billion (S$674 billion) in SDRs, which will be used as collateral. The GCMT will then borrow from the basket and then invest in mitigation projects and collect shares of the project returns. What projects to invest in will be up to the discernment of investment managers. Eventually, Persaud projects that the GCMT will draw US$3-4 trillion (S$4.04-5.39 trillion) in private savings.

“[the trust] is not on the developing country balance sheets, [the trust] is not even on the developed country balance sheets, it is a third balance sheet to fund projects, not governments.”

To him, the idea of a third balance sheet for global public goods would be much-needed to ease the global cost of capital.

Political Double Movement

On trusts and financial institutions, Ali called for their wholesale politicisation. She wants to demystify the neutral position of institutions like the WB and IMF and pull back the proverbial curtain. She asks, “there’s $700 billion (S$943 billion) unused at the World Bank, they’re hanging on to their AAA rating. How about letting that go a notch so that they can lend more?”

Gelpern agrees, “I actually don’t think the World Bank would lose anything with the credit ratings. And if anything, you know, ratings agencies think they’re being too conservative.”

The Liberation of Agency

Moving on, Gelpern likens institutional reform to “moving the furniture around” and that “the really big problem is that we do not account for domestic politics, and for politics more broadly”. She reiterates that we cannot stop at a cleaning of the slate and crossing our fingers, hoping that the next day is brighter.

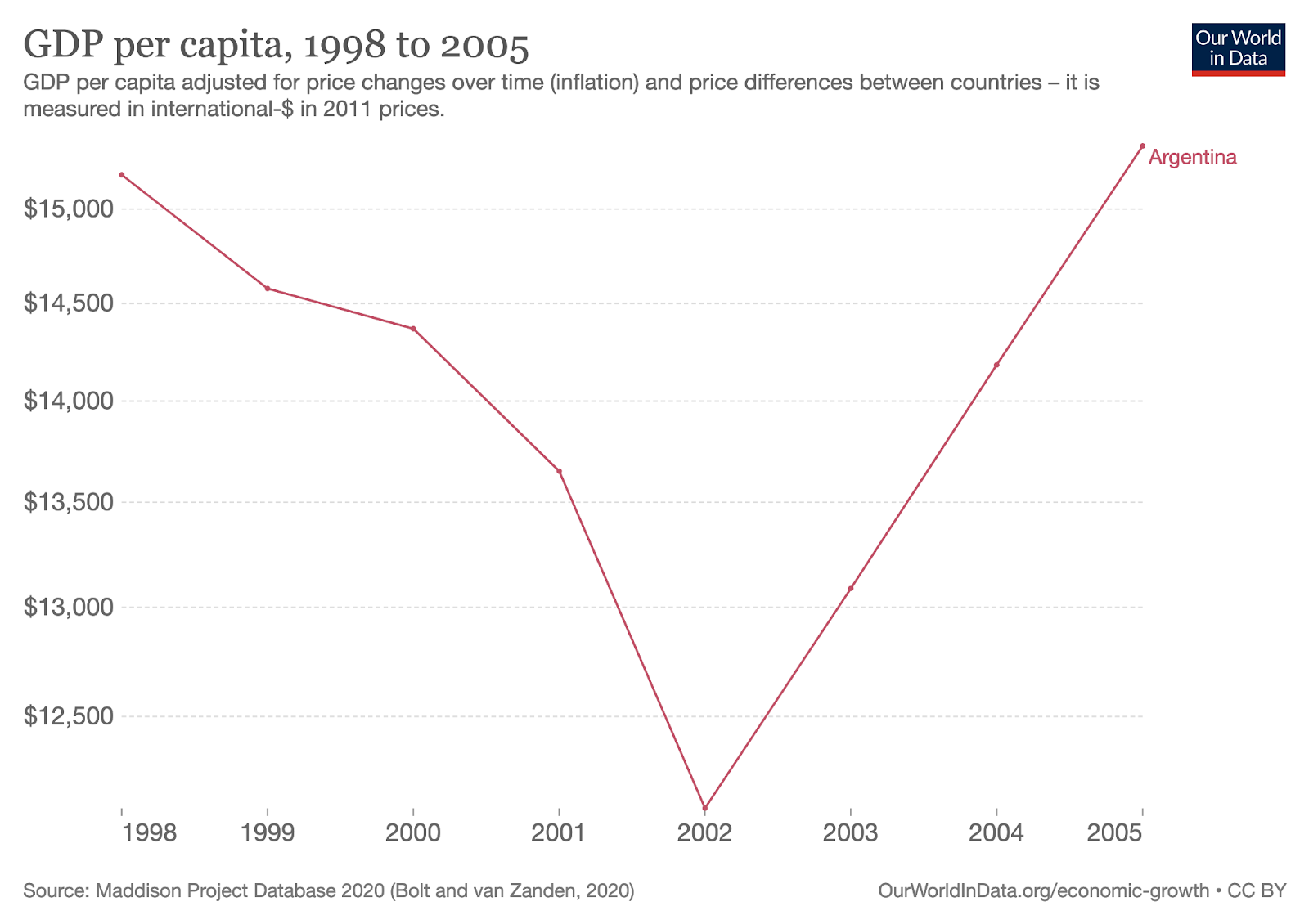

She brings up the example of Argentina who, in her and Setser’s account, had solved their debt crisis in the late 1990s by fixing their internal policies. They did not rely on the IMF.

Here, I am in complete agreement. The structural factors affecting our planetary survival certainly plays an outsized factor. However, deferring it to the large brush strokes of history is simply not a useful framework.

When I think of agency I think of Robin Wall Kimmerer’s Braiding Sweetgrass. Deferring the responsibility of solving for stability to structural factors can be suffocating. Nothing will ever change if nations simply waited for large scale reforms to happen, even if the polycrisis is a collective action problem. This learned powerlessness can be intoxicating. Kimmerer contemplates, as we are primed to perpetual dread, “[o]ur natural inclination to do right by the world is stifled, breeding despair when it should be inspiring action.”

To sum up, there seems to be three broad themes that the panel had covered: one, transfers in the form of SDR distribution and trusts; two, bail-ins in the form of debt cancellation; three, fiscal consolidation. Tying these all together is the idea of agency. As Kimmerer tells us, “It is, of course, dead bodies that build soil, that perpetuate the nutrient cycle that propels the living.” Agency reminds us that we can and must take action, even if it seems like it may be too late.