‘The Pearl of the Indian Ocean’—that was one of the nicknames given to Sri Lanka, an island off the southeast coast of India.

Throughout history, Sri Lanka has boasted a reputation of being an important trading hub, whether during the time of the ancient Silk Road or during World War II. In 2015, the nation was named a key node in the Maritime Silk Road as part of the ‘One Belt, One Road” initiative’, which would greatly facilitate China’s overseas trade. This attracted large investments from China, amounting to US$12.1 billion (S$16.99 billion) between 2006 and 2019.

The country’s economy is also dominated by the exports of its well-known Ceylon black tea, as well as coffee, gemstones, coconuts, rubber and cinnamon.

Aside from its trade capabilities, Sri Lanka is a popular tourist destination—named as the ‘Best Emerging Destination for 2019’ by Trip Expert, a leading international travel agent. In fact, Sri Lanka’s tourism sector is a national heavyweight, contributing a hefty 12.6 per cent of the country’s overall Gross Domestic Product (GDP) in 2019 and accounting for up to two million employment opportunities.

However, despite the many advantages Sri Lanka possesses, economic challenges have plagued the country continuously. Over the years, these problems snowballed, eventually leading Sri Lanka to declare bankruptcy in July earlier this year. The announcement culminated in an economic crisis that would be labelled the country’s worst modern economic crisis since 1948. Not only that, but the economy’s downfall had quickly plunged the country into political turmoil, with things coming to a head when Sri Lankan protestors overthrew former President Gotabaya Rajapaksa that same month.

The economic emergency would disrupt the lives of Sri Lankans as they continued to struggle with food, medical and fuel shortages.

One may then ask, how is it that such a highly valued trading and tourism hub, rich with natural resources, went belly up?

The answer may lie with a deeper analysis of the Sri Lankan government’s actions, and the economic policy choices it made leading up to the crisis.

What happened in Sri Lanka?

On July 9, 2022, Sri Lankan protesters stormed former President Gotabaya Rajapaksa’s mansion, forcing the former president to flee and resign. This resulted from months of anti-government protests which began in April, in response to out-of-control inflation, shortages of food, fuel and medicine and surging costs of living. The repercussions of the crisis exacerbated the situation, with healthcare and power services being disrupted. Patients were denied treatment for illnesses as hospitals ran out of medical equipment and pharmaceuticals. Many Sri Lankans queued for days along fuel stations, hoping for supplies to return.

One of the main causes cited to have led Sri Lanka to its current state is the government’s mismanagement of its economy. Poor economic decisions compounded over the past three years, resulting in the depletion of the country’s foreign currency reserves by 99 per cent since 2019, and the government’s consequent inability to meet domestic demand for imports.

The ramifications of the Covid-19 pandemic and the Easter Sunday bombings months earlier did not help either, as both challenging events brought ruin to Sri Lanka’s former gold mine—its tourism sector—and hastened the demise of the economy.

Tracing Sri Lanka’s Downfall

Although Sri Lanka’s troubles appear to have had their inception when Rajapaksa’s administration introduced problematic tax cuts in 2019, the country has had an infamous track record of poor economic decisions from as early as the 1990s.

In fact, the current economic crisis may be traced to the mid-2000s, during which Sri Lanka was already in poor shape in terms of managing its debts. This was due to heavy reliance on commercial borrowing to fund its budget deficit at the time, as well as neglecting to find ways to increase government revenue. The government also missed opportunities to capitalise on their export market for better foreign exchange earnings.

The combination of these three mistakes set the stage for the disastrous consequences and eventual economic collapse in the years that followed.

2019: Tax Cuts Cripple the Economy

Addressing Parliament in May this year, Sri Lanka’s finance minister Ali Sabry called the government’s move of slashing taxes in 2019 a “historic mistake”.

One of the most significant changes implemented was the lowering of its Value Added Tax (VAT) from 15 per cent to 8 per cent. The minister explained that the intention was to “stimulate economic activity” and to “make use of that reinvigoration as a launchpad for the development of the country”.

This concept of lowering taxes to boost economic growth through enhancing disposable income and promoting the circulation of money in the economy is not new— there are many examples of countries which adopted this strategy successfully. However, in Sri Lanka’s case, reducing taxes had the opposite of the desired effect; around one million registered taxpayers were lost between 2020 to 2022. The government lost valuable revenue, and the country’s economy was further weakened.

In the months that followed, the COVID-19 pandemic would hit Sri Lanka while it was still reeling from the Easter Sunday bombings, and the situation would begin to spiral out of control. The tourism industry and other avenues for foreign exchange were badly affected. Many Sri Lankans lost their jobs due to the slew of pandemic-induced closures of hotels, airlines, travel agencies and shops, adding to public frustration. Exports, the number of loans and capital inflows into the country decreased while the demand for imports rose sharply. In just two years, Sri Lanka’s budget deficit rose from 9.6 per cent of GDP in 2019 to 12.2 per cent of GDP in 2022.

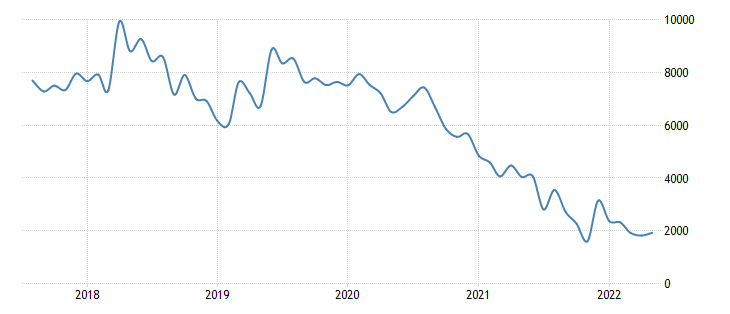

Lacking options, the government drew upon its foreign reserves to finance its debts. This resulted in a rapid decline in reserves from US$8.864 million (S$12.467 million) in June 2019 to US$ 2.361 million (S$3.320 million) in January 2022.

2021: Agricultural Reforms Devastate Local Production

The misfortune of President Rajapaksa’s administration did not end there.

In 2021, in an effort to reduce demand for foreign currencies as well as promote eco-friendly agricultural farming, the government proceeded to ban the import of agrochemicals. This decision proved to be catastrophic for Sri Lanka’s economy as it led to widespread crop failure.

Rice production dropped by 20 per cent within six months of the policy’s introduction, with prices shooting up by 50 per cent. The production of tea, Sri Lanka’s biggest export, fell by 18 per cent. The ban disrupted Sri Lanka’s self-sufficiency in rice production, causing them to even import rice from China and Myanmar to stave off a food crisis—and further draw upon FOREX reserves. By the time the policy was rescinded, Sri Lanka’s reserves dropped from US$4.06 billion (S$5.707 billion) to just US$1.92 billion (S$2.70 billion).

2022: Sri Lanka Defaults on Foreign Debts

On April 12 2022, the economic crisis would reach its peak, with Sri Lanka announcing it would be defaulting on $51 billion USD (S$71.66 billion) worth of foreign debt, and that it was in the process of discussing debt restructuring.

To understand how such a drastic conclusion was possible, it is worth analysing the components of the country’s debt.

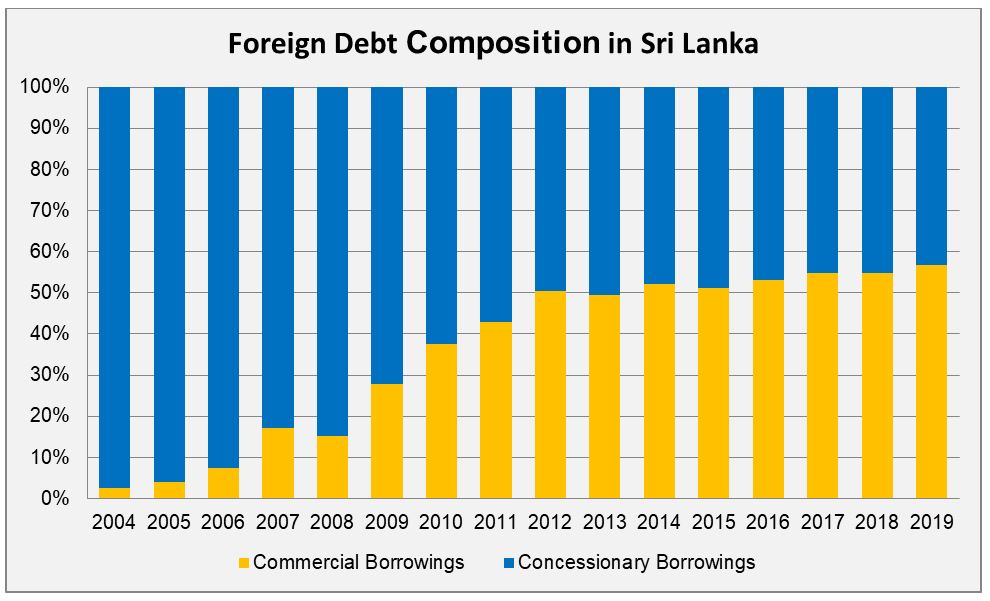

Sri Lanka’s foreign debt has its roots in loans taken from organisations such as the World Bank, Asian Development Bank and Japan International Cooperation Agency in the early 2000s. As a designated ‘low-income country’ at the time, it enjoyed favourable loan conditions, including low-interest rates and longer repayment periods. However, when the World Bank re-classified Sri Lanka as an ‘upper-middle income’ country in 2019, and a ‘lower-middle’ one in the subsequent year, the government had less access to concessionary loans. They began to change their external debt structure and leaned towards commercial borrowing in the form of International Sovereign Bonds (ISB) and loans from China. These loans, unlike their concessionary counterparts, have short payback periods, high-interest rates and no grace periods.

Recent years have seen Sri Lanka increase its foreign debt-to-GDP ratio from 30 per cent in 2014 to 42.6 per cent in 2019. This uncontrolled borrowing for infrastructure projects weakened the economy even further in the years leading up to the crisis.

What’s next for Sri Lanka?

On September 1st 2022, the International Monetary Fund (IMF) preliminarily agreed to extend a 48-month rescue loan of US$2.9 billion (S$4.08 billion) under its Extended Fund Facility to aid in the recovery of Sri Lanka’s economic stability. Under the deal, funds would be provided to Sri Lankan authorities on the condition that the government makes arrangements with creditors for the restructuring of its debts, as well as provides assurances that structural reforms would be put in place to address corruption vulnerabilities. The United States also announced it would be providing US$40 million (S$56.251 million) of agricultural aid to Sri Lanka for the purchase of fertiliser for its next harvest season.

Speaking at a press conference, IMF’s Mission Chief Peter Breuer said that the preliminary agreement showed that Sri Lanka is “serious in engaging in reforms” and urged creditors to cooperate with Sri Lanka through this process. He highlighted a few specific conditions of the deal: rebuilding foreign reserves, implementing tax reforms with the aim of achieving a GDP surplus of 2.3 per cent by 2025, improving social safety net programs, and introducing cost-recovery pricing for fuel and electricity. He also added that if the reforms are successfully implemented, it would create a “catalytic effect” which would bring investments back into Sri Lanka.

Sri Lanka has already taken steps to fulfil the conditions of the loan, hiking value-added tax back to 15 per cent. With the appointment of the new President Ranil Wickremesinghe, there is also some sense of normalcy back in Sri Lanka, and public unrest has quietened.

Wickremesinghe has also since unveiled his administration’s first budget proposal for economic recovery, which would strive to increase government revenue by nearly 15 per cent of Sri Lanka’s GDP by 2025, subsequently slashing public sector debt and keeping inflation in check. Meanwhile, a proposed bid to introduce multiple entry tourist visas would seek to boost ‘repeat tourism’ and revive the industry.

Sri Lanka may even optimistically expect one million tourists by the end of this year and generate expected tourism revenue of US$1.8 billion (S$2.53 billion). While such a figure may pale in comparison to the 2.3 million tourists that visited Sri Lanka in 2018, it serves to indicate that the recovery of the tourism industry is underway and that the Sri Lankan government is working to bring stability back to the country.

With time and lessons learnt from past mistakes, Sri Lanka may be on the right track to reviving its economy and restoring itself to its former glory.